Many Americans are nearing retirement age or even starting retirement. While there are many notable exceptions, as a generation Baby Boomers have made great incomes during their careers but have not saved enough for retirement. Many plan to work longer or really never stop working. Unfortunately, there is not always a choice as many are finding themselves laid off

in their late fifties or early sixties.

(Note, if you click on a link in this post and buy something from Amazon (even if you buy something different from where the link takes you), The Small Investor will receive a small commission from your purchase. As an Amazon Associate I earn from qualifying purchases. This costs you nothing extra and is the way that we at The Small Investor are repaid for our hard work, bringing you this great content. It is a win-win for both of us since it keeps great advice coming to you (for free) and helps put food on the table for us. If you don’t want to buy something from Amazon or buy a book, how about at least telling your friends and family about our website as a great place to learn about investing and personal finance. Thanks!)

Note that retirement is a relatively new issue since, with a life expectancy of 67 years, many in past generations died soon after stopping work. There was little need to worry about funding a 30-year retirement. Today some individuals are living to age 90 or longer. Others are running out of money and finding the need to return to work after a short retirement. Such is the case for a former Oral-B vice president. Despite a six figure income during his working career, he had only $90,000 at retirement. His nest egg was not able to weather the 2008 financial crisis, forcing him to return to work.

Pensions are gone

Another benefit that many in past generations had were pension funds. Pensions provided a monthly stipend for the rest of your life after you reached retirement age. Sometimes the company would just fund these entirely and all you would need to do was put in a certain number of years of service to the company. Other times employees would make a contribution as well, but the company would kick in extra money to increase the benefit.

Unfortunately, pension funds were handled badly by companies. Just as many individuals will do when expected to take care of their own retirement investing, many companies didn’t fund pension plans they way that they needed to do because the need for the money was far off and there were pressing, current needs. When the stock market did well, the company directed money to other needs. This was fine when the markets were doing well, but when bear markets came, there was no money in the budget for the pension fund. Executives also promised more and more lavish benefits to make workers happy because it was easier to promise something thirty years down the road than it was to pay out raises now.

As a result, companies have decided that it is better to pay a fixed amount now in what is called a defined contribution plan, rather than promise to pay out a certain amount later in what is known as a defined benefit plan. The company will put a certain amount into your 401k plan now, but when retirement comes, whatever is there is what is there. You’ll need to put in enough to make up the difference. And managing the money between now and then is up to you.

Becoming your own pension fund manager

As a result, individuals need to become their own pension fund manager. They need to make sure they’re contributing enough, invest it properly, and then use the money they have to generate the income needed in retirement to pay their bills. Plus, they’ll need to make sure they don’t take out too much too soon and run out of money. Oh, they also need to worry about keeping up with inflation. If all this sounds tough, well, it is.

But if you do it right, you’ll actually find that you have a greater income and greater flexibility with your money than you ever had with a traditional pension plan. You’ll also have more money to give to your kids or your favorite charity when you die. So how can one prepare to weather a long retirement? The secret is a combination of a large amount of savings, making the right investments, and keeping your liabilities in check.

How much will you need?

The first step in preparing for retirement is determining how much you’ll need. In FIREd by Fifty: How to Create the Cash Flow You Need to Retire Early, a methodology is developed to determine both how much you’ll need for retirement (whenever you decide to retire) and how much you’ll need to be putting away each month to reach that goal by a certain age. A good first estimate is to assume you’ll need 90% of your current salary, then multiply that number by 30. So, if you make $80,000, you’d multiply:

$80,000 x 0.90 x 30 = $2.2M

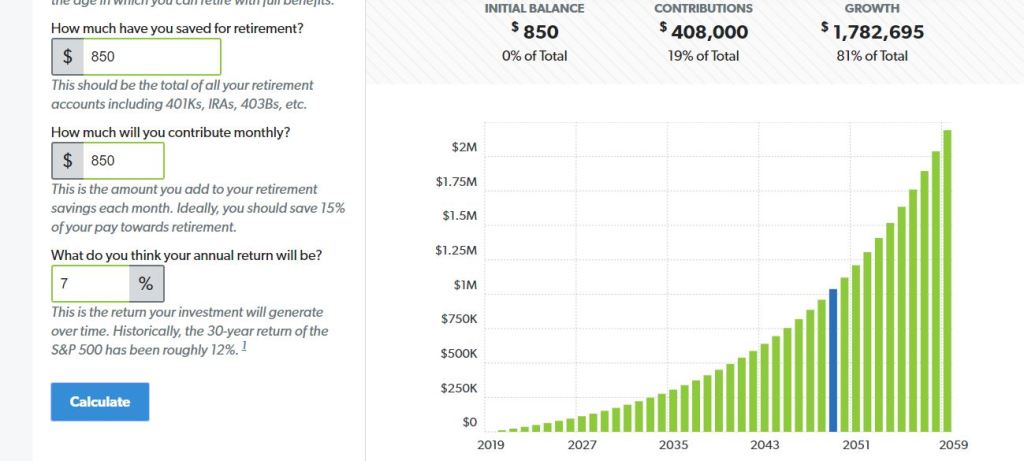

To determine how much you’ll need to put away each month to get there, a good strategy is to use an investment calculator. For example, if I use this one and assume a rate-of-return of 7% (which is a good assumption for your return from a stock portfolio when you include inflation), I find that I need to contribute about $850 per month to reach $2.2M in 40 years. Note that this is about 12.8% of the $80,000 salary. If you put away 15%, between your contributions and those of your employer, you should be contributing a little more than you will need.

Your Savings.

Most of the investing you’ll do within a 401k will be using mutual funds and, perhaps, ETFs. Investing with mutual funds really isn’t that hard, but you’ll need to know the basics to generate the 7% after-inflation returns you’ll need to hit your goals. A great book for learning about investing with mutual funds is The Bogleheads’ Guide to Investing. In particular, The Bogleheads recommend using index mutual funds due to their low fees.

Managing your money in retirement

Cash. Because you’ll have no source of income beyond your investments (including pensions), you’ll need to keep more cash on hand than you did while you were working. When you had a paycheck coming in your could afford to wait when the market swooned. In retirement, you’ll still have bills to pay regardless of how the market is doing. For this reason you’ll need to keep a savings of at least 3-5 year’s worth of expenses in liquid assets such as bank CDs and money market funds, preferably spread out among a couple of banks. These can be structured with a few month’s worth of savings in a money market fund, another years worth of savings in a 6 month CD, and then the rest in a one year CD (or even a longer term CD for some of the funds).

Income assets. If you have income producing assets, such as bonds or dividend paying stocks, these can be used to rebuild your savings. Bonds typically pay interest payments twice per year, while stocks pay dividends quarterly. These payments can be directed into a money market fund and either be used to purchase CDs as income builds or to refill short-term savings, allowing the longer term CDs to be rolled over as they mature. In an ideal situation there would be plenty of income from bonds and income stocks to pay for all regular expenses.

Growth Investments. While you’ll be using more of your money to generate income to meet expenses, you’ll still need growth. You should expect the amount of income you’re getting from bonds and other income assets to be relatively fixed. This means that if you’re getting $20,000 from your bond portfolio when you retire at age 65, you should expect to still be getting $20,000 from it at age 85. Meanwhile, it is likely that things will cost about 70% more by that time.

Dividend-paying stocks will increase their payout over time and largely keep up with inflation, provided you aren’t buying something like preferred shares of stock where the dividends are fixed. The issue is that stock dividends tend to provide a lower return than bond interest, so you’ll likely need to include a fair percentage of bonds to generate enough income.

You will therefore need to have some money in growth assets which you will sell off over the span of your retirement and use to buy additional bonds and other income assets. You cannot afford to take the risks you took when you were younger with your investments. A big loss now may never be regained. The rule therefore is diversification. In addition to having a generous portion of income producing assets, you’ll need to have your stock investments spread out among a wide array of assets. This means having mutual funds invested in different segments of the market (large caps, small caps, and international). You also might wish to have some real estate exposure, either directly with rental properties or through REITs.

Should you hold individual stocks at all?

Your tolerance for having investments in individual stocks depends on the size of your portfolio. If you only have 5-10 times your needed annual income saved, individual stocks might be too risky. If you have 20 times your income saved, you have more latitude since you’ll be able to wait for your portfolio to recover.

In fact, the more money you have saved and invested, the less cash you’ll need to keep on hand and the more risk you can take. Even if you suffer a rather large loss in percentage terms, if you have a large nest egg you’ll still have plenty of money to meet expenses. The ability to take on extra risk translates into more retirement income. While this advice won’t help you much if you’re 59 with retirement around the corner, think about investing more for retirement if you’re in your twenties.

You can learn a lot more about individual stock investing in SmallIvy Book of Investing: Book1: Investing to Grow Wealthy.

Your Expenses. Lower expenses translate into a lower required income. All loans should be paid off long before you’re entering retirement. (Ideally they would be paid off before your kids are ready to enter college.) You should think about downsizing your home to lower maintenance

and air conditioning costs. Moving to areas with a lower cost of living is also a consideration.

Realize that you will see expenses that you didn’t have earlier in your life. You’ll likely be taking different prescriptions and seeing the doctor more regularly. This may very well eliminate much of the savings you have from not having a mortgage bill. Remember to budget this in when determining your income needs.

Have a burning investing question you’d like answered? Please send to smallivy@smallivy.com or leave in a comment.

Disclaimer: This blog is not meant to give financial planning or tax advice. It gives general information on investment strategy, picking stocks, and generally managing money to build wealth. It is not a solicitation to buy or sell stocks or any security. Financial planning advice should be sought from a certified financial planner, which the author is not. Tax advice should be sought from a CPA. All investments involve risk and the reader as urged to consider risks carefully and seek the advice of experts if needed before investing.