A budget is like your GPS app. You tell it where you want to go and it figures out a way to get there. There are basic budgets where you just make sure you don’t spend more than you make each month. There are then more complicated cash flow plans as described in FIREd by Fifty: How to Create the Cash Flow You Need to Retire Early that take into account future needs like saving for retirement and investing for the next new roof for your home. The basic budget makes sure you don’t run out of money before the end of the month, where the cash flow plan helps you build up wealth and avoid debt by using your money wisely. The basic budget is like a trip down the street to a friend’s home where you just need to know how to get there, where the cash flow plan is a trip across country, including where you’ll stay for the nights and where you’ll get food and gas.

(Note, if you click on a link in this post and buy something from Amazon (even if you buy something different from where the link takes you), The Small Investor will receive a small commission from your purchase. As an Amazon Associate I earn from qualifying purchases. This costs you nothing extra and is the way that we at The Small Investor are repaid for our hard work, bringing you this great content. It is a win-win for both of us since it keeps great advice coming to you (for free) and helps put food on the table for us. If you don’t want to buy something from Amazon or buy a book, how about at least telling your friends and family about our website as a great place to learn about investing and personal finance. Thanks!)

But if you ignore your GPS app, you’ll still get lost or at least not get where you wanted to go. If you ignore your budget or your cash flow plan, you won’t get to where you want financially. But unlike a GPS, unless you have an budgeting app like Mint that follows your spending and tells you when you’re overspending in some area, a budget won’t even tell you you’re off route. Most budgets are a piece of paper or a spreadsheet on a computer, so you won’t even know you’re going off budget unless you check it regularly and really track your spending in each category. Sure, you can recalculate when you do check and find that you’re off plan, but it is better to stay on your budget so you don’t have the hassle and stress of getting back on plan. Today we’ll give some strategies to help stick to your budget without a lot of effort.

Types of expenses

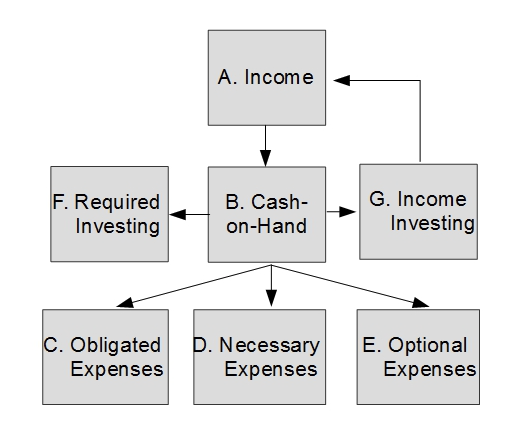

As detailed in FiREd by Fifty, there are different kinds of expenses. These are shown as items C through E in the cash flow diagram below. The way you handle each of these expenses and stay on budget is somewhat different. For some, you use automated tools such a automated money transfers. For others, you may use cash to avoid overspending or be very diligent and track your spending as you go. For others they just are what they are, but you learn how much you expect to pay each month and adjust your behavior to stay at around the right level.

Items F and G aren’t really expenses, but are an important part of a cash flow plan and should be included in a budget. Item F is investing for big life events like retirement. Item G is investing in stocks, bonds, and real estate to generate income that you can then use to increase the amount of money you have available. It is also a storage of wealth for future expenses so that you’ll have cash for things like the next car you buy. You’ll want to make sure you’re following your plan to put this money away as well since it will make it easier and easier to buy things as this portion of your wealth grows.

We just started using PrettyLitter and are liking the results, so I became an Affilliate! PrettyLitter traps odor instantly and then eliminates moisture, so you’ll never smell your cat’s dirty business again. Easier cat care and fresh litter is just around your doorstep. No need to add baking soda for extra odor absorption. Ditch the pine pellets and upgrade to silica cat litter!

C. Obligated Expenses

Obligated expenses are things like your apartment rent, home mortgage, or car payment. You are required to pay for these things each month and really can’t adjust them. Most obligated expenses are fixed in price, so they are easy to plan for. For example, if your rent is $1000 per month, you’ll need to put away $1000 per month for rent.

The best way to make sure you stay on track with obligated expenses is to just pay them as soon as you can when you get paid and have the money available. In some cases you may need to split them and pay some at different times when you have the money. For example, you pay your rent with the second paycheck for the month and pay your car payment with the first paycheck if you get paid twice per month. You might also have a separate checking account where you put away the money for these expenses so that it doesn’t get spent or, if you have the discipline, have a certain portion of the money in your checking account off-limits because this is the money you’ll need for obligated expenses. For example, maybe you know when you’re taking care of other expenses that you don’t let your balance drop below $2000 until you’ve paid your obligated expenses because that money is already obligated. If you have a savings and a checking account, maybe you put the money for these expenses into savings (or have your paycheck deposited into savings, then transfer the money to checking right before you pay the bills). That way you know that all of the money in your checking account is available to spend without spending the rent money.

Realize that you should always have some money tucked away in an emergency fund. This is money you don’t spend unless there is some sort of expense that is unexpected and needs to get paid right away. If you ever spend any of this money, you’ll need to replenish it as fast as you can. This money then gives you some float to cover obligated expenses should something unusual come up during a month. The money you’ll eventually have in your income investments is an even better place to use as a float to cover things, letting you leave your emergency fund untouched more often. When you are just starting and haven’t built up a big income investing account yet, however, you’ll probably need to use your emergency fund periodically.

D. Necessary Expenses

Necessary expenses are things like food, clothing, and electricity. You need them to survive, but the cost can vary from month to month and you have the ability to spend more or less through your choices. This makes it necessary that you keep your budget in mind when buying needed things.

Things are like utilities are fairly easy to control, or really to predict. Your utility bills for a given season of the year will usually be fairly constant. You might see a bill increase or decrease in months where you need to run the AC a lot or the heater. Water might be higher as well in the summer when you’re watering gardens or in December if you have a lot of guests, taking baths. But these changes can all be estimates with a little experience and included in your monthly budget. You can also find the average amount you spend (or the yearly amount) by saving your bills for the first year or two and then budget that amount for the year. You need to build up extra cash during the low utility months, knowing that the high utility months were coming. You’d just put this cash into savings so it doesn’t get spent on other things before the high utility months come. Note that you can cut your utility bills somewhat through your behavior, which is something to look at if you need to free up a little cash. These are things like setting the thermostat lower in the winter and wearing more clothes.

Necessary expenses like clothes have a lot of flexibility and can be predicted. The best way to control these is to have a preset budget and do your clothes shopping intentionally. By this, I mean that rather than wandering through stores, looking to see what’s on sale and impulse buying, set aside money each month (or better, a couple of times per year), give yourself a budget, then see what you need and go to the store to buy just those items. When you go, have your budget in mind or take cash. Definitely look for sales to stretch your money, but don’t let them cause you to buy things you don’t need right now. If you find things are under budget, don’t buy more just because you have the money. Save the extra up for later in the year when things are over budget. Other household things are like clothing where you have a fixed budget and buy them when needed.

Things like food are the easiest to abuse because there is such a wide range of what you can pay. You can eat at home for $3 per meal or easily spend $30 or more at a restaurant. For food, you need to plan both how you’ll eat and your budget. Certainly you should go out to eat periodically, but plan when you’ll go out and how often and have a budget for how much you’ll spend when you do. And bring cash if you can when eating out since that is the simplest way to avoid overspending.

At home, plan your meals and buy just what you need for those meals, then actually make those meals when scheduled unless it is unavoidable. Avoid shopping when you’re hungry since this will cause the most impulse buying. If you find that you have a lot of extra uncooked food left over that builds up over time, try to plan future meals to use those ingredients so they don’t spoil. in general, plan the same meal a couple of weeks in a row so that you can buy in larger quantities but use up ingredients. Also realize that leftovers from dinner at home (or from a restaurant) make great lunches the next day at work, so cook an extra portion and wrap it up when you’re done.

Some people use an budget envelope system where they use cash for basically all of their necessary expenses including groceries and clothing. Each month, or twice a month, you withdraw what you’ll need in cash from the bank for each necessary expense and put the money in its envelope. When the envelope’s out of cash, you’re done for that category. I find this a little too cumbersome, but I do use cash for things like eating out and other entertainment.

Because we now have ready access to bank account information, you can do a fairly good job of tracking your spending as you go even if you’re using a debit or credit card to make the purchases. This gets more difficult the smaller the purchases are, but can work if you’re only shopping a couple of times a month for some items. Just know your budget for each category is and then deduct what you spend when you get home from what you have for the month. Then, the next time you shop for that category, review what you have left before you go and watch your spending accordingly. When you’ve spent up to your limit for the month, stop buying in that category. Printing out a copy of your budget to mark up as you go or using a spreadsheet where you enter your spending as you go can help with this tracking. Again, there are also apps like Mint that do tracking by category automatically.

Want to learn a lot more about stock investing?

If you want to go from being one of the crowd to a sophisticated investor, pick up a copy of SmallIvy Book of Investing: Book 1: Investing to Become Wealthy. In there I explain a lot more about things like growth and income investing. Having this kind of knowledge will help you get that extra edge you need to best your peers. There is also lots of material on how you should be managing your money at different stages of your life to grow your wealth. Please consider grabbing a copy and checking it out. I think you’ll be glad you did.

E. Optional Expenses

Optional expenses are luxuries. Certainly, every budget should contain luxuries even if it is just an ice cream cone or an Espresso coffee drink a couple of times per month. As you get to higher income levels, both from work and if you’re putting money away in income investing (Box G), you can also afford some bigger luxuries like lavish vacations and fancy cars and boats. But luxuries require the most control because they can easily get out of balance and blow your budget.

There are two categories of luxuries, big and small. Big luxuries should be saved up for and purchased with cash (no loans). If you need to buy a boat or sports car on payments, you can’t afford it. Save and invest for it or start out used and cheap and trade your way up. Any recurring costs for luxuries should be considered and budgeted in your luxury category. Ideally you should have an income investment such as a mutual fund that is tied to the recurring costs of a luxury. For example, you invest in a mutual fund and then receive dividends or sell off small portions each year to pay for maintenance and dock fees on your yacht.

This is a great book I’d recommend on mutual fund investing:

Having investments specifically for vacations, and then using a specified percentage of that investment (such as 10%) each year as your vacation budget is a great plan. This is accomplished by putting some of the money you were planning to spend on vacation the first few years in a mutual fund that you specifically buy to fund vacations in the future instead and taking a smaller vacation with the rest of the money. In the early years you add to the investment each year to increase how much you can spend on vacations in the future. This means you’ll probably start out small, but you’ll be surprised at what you’ll have the cash for in ten or twenty years if you limit how much you take out and add some cash periodically in the early years.

Small luxuries are things like an extra meal out or some impulse buy from a store. For these expenses you should have a budget each month of “blow money.” This is money you should take out in cash each month (or that are carefully tracked if using a debit card) that you are free to spend on whatever you want, no questions asked. When the money is gone, it’s gone and you’re done with impulse buying.

F. Required and G. Income investing

Required investing is things like retirement investing and putting away money for your children’s college. Putting money away in a health savings account (HSA) while you’re young and healthy, if one is available through your work, is another great thing to do that will pay great dividends in the future since you’ll have the money you need for future expenses and all of that money (and the growth) will be tax-free. This type of investment should be automated where money is taken out of your check before you even see it. I generally don’t even include this money in my budget since I never see it. I just choose an appropriate amount (like 10-15% of income into retirement), set it up with my employer, then forget about it.

If you don’t have employer sponsored accounts like a 401k or you wisely want to invest through accounts like IRAs where you have more control and investment options, you can still automate. Most brokerages have tools that let you create automatic transfers from your checking account. Just set them up to take out the money right after you get your paycheck and it will all be taken care of for you. If you setup the money to be invested automatically on the other side, you won’t need to worry about it much at all.

Income investing takes a little more doing. These are investments in a taxable account. When you first start, you’ll just invest this money and let any income or growth be reinvested. As it grows, you’ll be able to start taking some money out of this account. Usually this will be cash to buy one-time luxuries or make big needed purchases like a home repair, but once the account is large enough you can use it to supplement your regular work income.

If you find that you’ll have a certain amount of free cash flow (cash left over after you pay for everything) each month, you can automate investments into your income investment accounts as well. Remember if you’re doing this that there will be some months where you have bigger expenses, so you’ll need to be sure that you don’t invest money you need later in the year. (Realize that investing for short periods of time is a crap shoot where you don’t know how you’ll do, so money you’ll need during the year should be left in cash.) A good way to do income investing is to either let your cash build up in your checking and savings until it is high enough that you know you’re be able to cover everything and then invest the extra or use special paychecks and bonuses for income investing. As an example of the latter, if you get an extra two paychecks each year because you get paid 26 times (every two weeks), during the two months when you get the extra paychecks, put some of that money into your income investments.

Once your income investments reach a certain threshold, you really won’t need to contribute more. You can just let some of the income they generate roll-over and they will continue to grow. As long as you don’t spend from them at too great a rate, they will continue to grow and always be there to support you.

Have a burning investing question you’d like answered? Please send to smallivy@smallivy.com or leave in a comment.

Disclaimer: This blog is not meant to give financial planning or tax advice. It gives general information on investment strategy, picking stocks, and generally managing money to build wealth. It is not a solicitation to buy or sell stocks or any security. Financial planning advice should be sought from a certified financial planner, which the author is not. Tax advice should be sought from a CPA. All investments involve risk and the reader as urged to consider risks carefully and seek the advice of experts if needed before investing.